Over the past six months, Yum China’s shares (currently trading at $43) have posted a disappointing 17.8% loss, well below the S&P 500’s 15.7% gain. This might have investors contemplating their next move.

Is now the time to buy Yum China, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Yum China Not Exciting?

Even with the cheaper entry price, we don't have much confidence in Yum China. Here are three reasons you should be careful with YUMC and a stock we'd rather own.

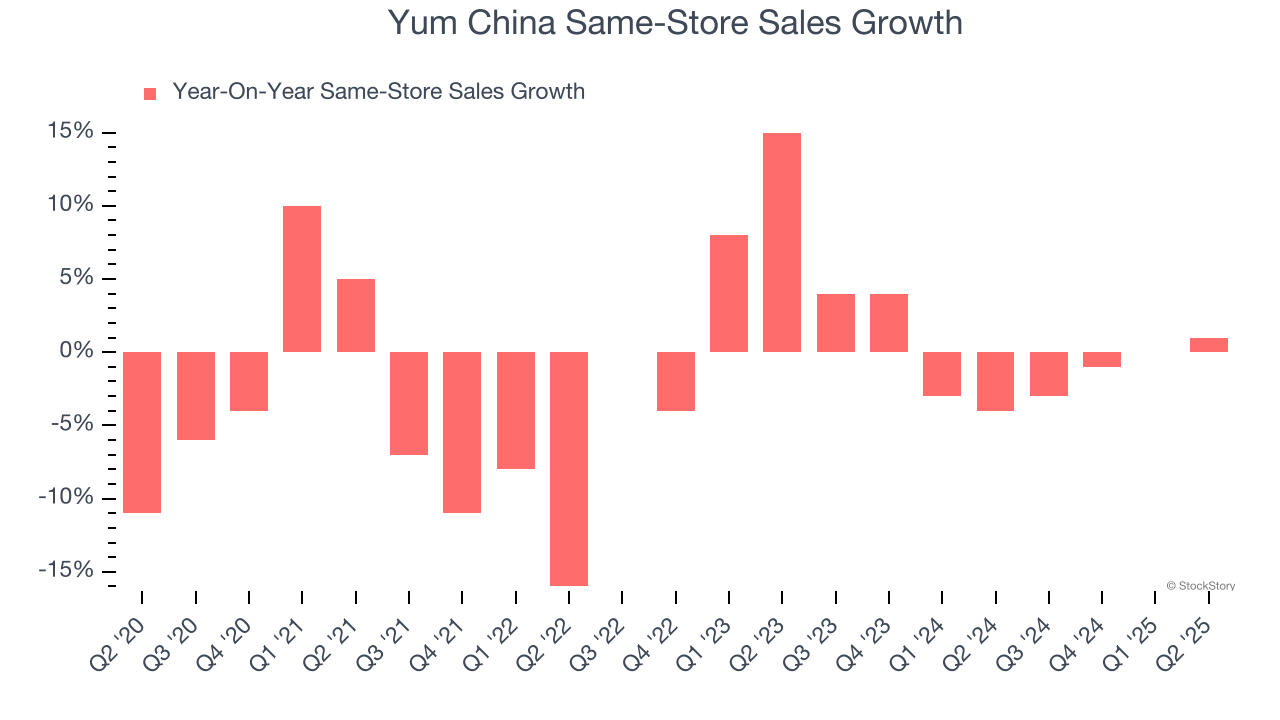

1. Flat Same-Store Sales Indicate Weak Demand

Same-store sales is an industry measure of whether revenue is growing at existing restaurants, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Yum China’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat.

2. Projected Revenue Growth Is Slim

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Yum China’s revenue to rise by 4.8%, close to This projection doesn't excite us and suggests its newer menu offerings will not lead to better top-line performance yet.

3. Low Gross Margin Reveals Weak Structural Profitability

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate pricing power and differentiation, whether it be the dining experience or quality and taste of food.

Yum China has bad unit economics for a restaurant company, giving it less room to reinvest and grow its presence. As you can see below, it averaged a 20.1% gross margin over the last two years. Said differently, Yum China had to pay a chunky $79.89 to its suppliers for every $100 in revenue.

Final Judgment

Yum China isn’t a terrible business, but it isn’t one of our picks. After the recent drawdown, the stock trades at 15.7× forward P/E (or $43 per share). This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are more exciting stocks to buy at the moment. We’d recommend looking at the most dominant software business in the world.

Stocks We Like More Than Yum China

Trump’s April 2025 tariff bombshell triggered a massive market selloff, but stocks have since staged an impressive recovery, leaving those who panic sold on the sidelines.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.