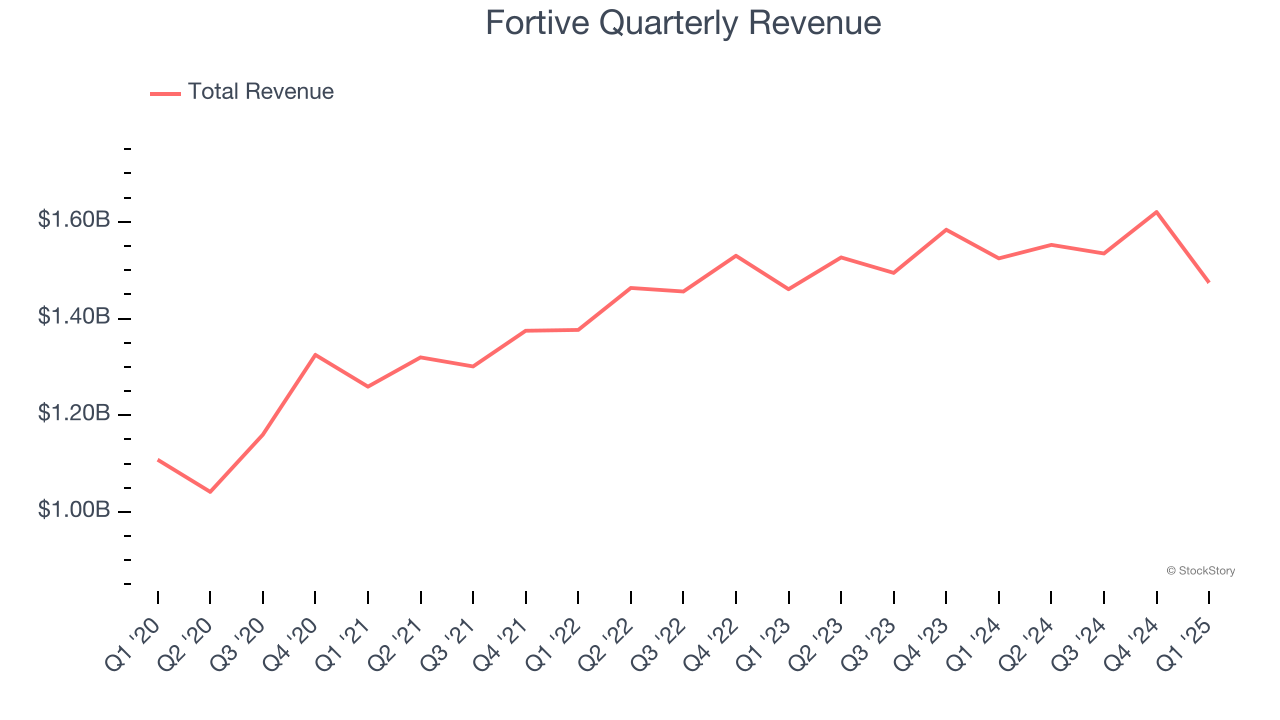

Industrial technology company Fortive (NYSE:FTV) fell short of the market’s revenue expectations in Q1 CY2025, with sales falling 3.3% year on year to $1.47 billion. Its non-GAAP profit of $0.85 per share was in line with analysts’ consensus estimates.

Is now the time to buy Fortive? Find out by accessing our full research report, it’s free.

Fortive (FTV) Q1 CY2025 Highlights:

- Revenue: $1.47 billion vs analyst estimates of $1.50 billion (3.3% year-on-year decline, 1.4% miss)

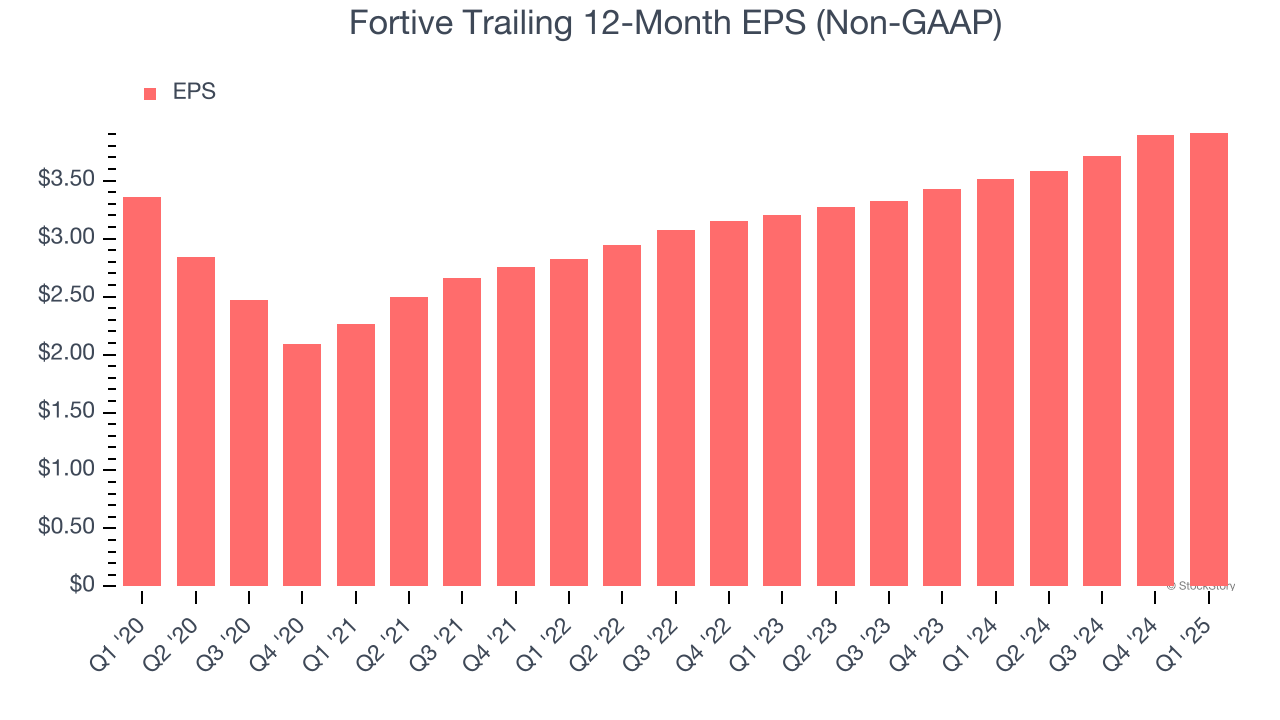

- Adjusted EPS: $0.85 vs analyst estimates of $0.85 (in line)

- Management lowered its full-year Adjusted EPS guidance to $3.90 at the midpoint, a 3.9% decrease

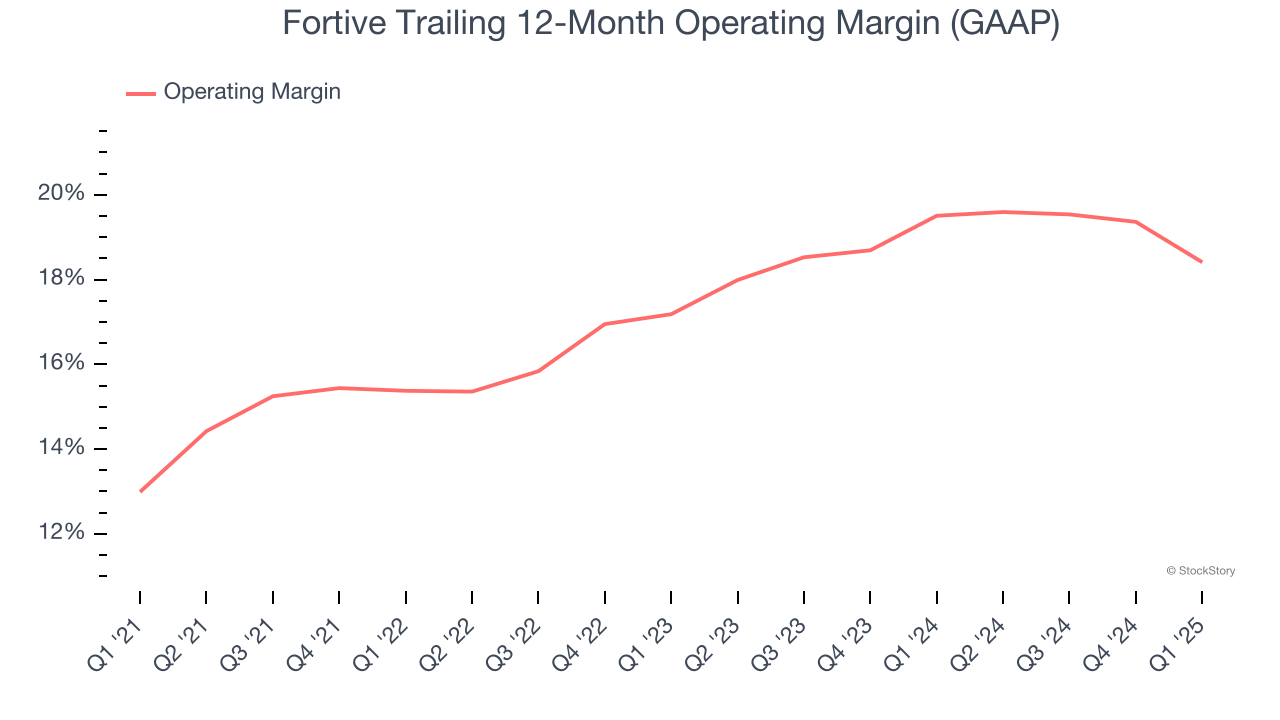

- Operating Margin: 15.8%, down from 19.8% in the same quarter last year

- Free Cash Flow Margin: 14.6%, similar to the same quarter last year

- Market Capitalization: $23.69 billion

James A. Lico, President and Chief Executive Officer, stated, “Our first quarter results reflect our continued ability to adapt and respond to the current dynamic macroeconomic environment. We delivered core growth in our Intelligent Operating Solutions and Advanced Healthcare Solutions segments, supported by solid demand for our industry-leading portfolio of safety and productivity solutions. Our Precision Technologies segment saw customers in test and measurement delay investments in light of increased geopolitical and macroeconomic uncertainty, while strong demand continued for utility monitoring and defense & space solutions. Rigorous operational execution contributed to continued margin expansion and strong free cash flow generation in the quarter.”

Company Overview

Taking its name from the Latin root of "strong", Fortive (NYSE:FTV) manufactures products and develops industrial software for numerous industries.

Sales Growth

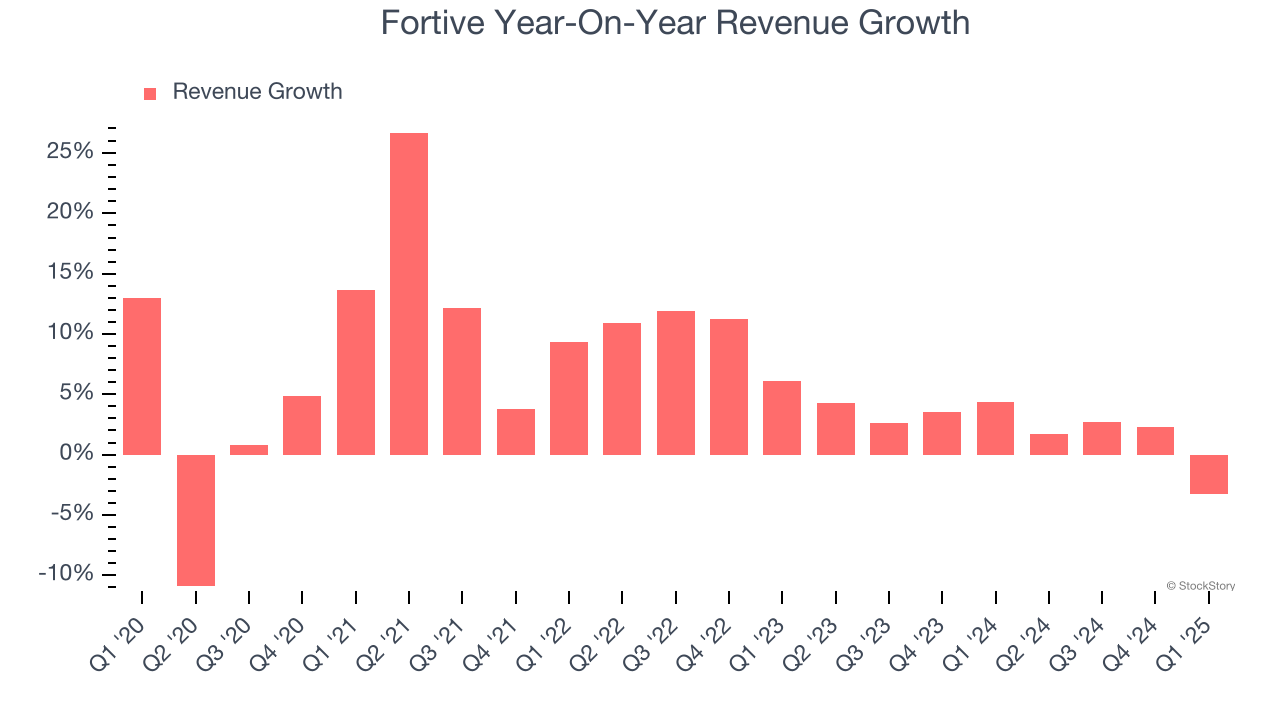

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Fortive’s sales grew at a tepid 5.7% compounded annual growth rate over the last five years. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Fortive’s recent performance shows its demand has slowed as its annualized revenue growth of 2.3% over the last two years was below its five-year trend.

This quarter, Fortive missed Wall Street’s estimates and reported a rather uninspiring 3.3% year-on-year revenue decline, generating $1.47 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and implies its newer products and services will not accelerate its top-line performance yet.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Fortive has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Fortive’s operating margin rose by 5.4 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Fortive generated an operating profit margin of 15.8%, down 4 percentage points year on year. Since Fortive’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Fortive’s EPS grew at a weak 3.1% compounded annual growth rate over the last five years, lower than its 5.7% annualized revenue growth. However, its operating margin actually expanded during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

We can take a deeper look into Fortive’s earnings to better understand the drivers of its performance. A five-year view shows Fortive has diluted its shareholders, growing its share count by 1.4%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Fortive, its two-year annual EPS growth of 10.6% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q1, Fortive reported EPS at $0.85, up from $0.83 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Fortive’s full-year EPS of $3.91 to grow 4.6%.

Key Takeaways from Fortive’s Q1 Results

We struggled to find many positives in these results. Its EPS guidance for next quarter missed significantly and its full-year EPS guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 5.1% to $66.05 immediately following the results.

The latest quarter from Fortive’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.